The very best and obvious example of what this article of McKinsey’s is all about, would be with how the Shale Gas impacted conventional oil, more specifically how the Impact of U.S. Shale Oil Revolution on the Global Oil Market has come to be the latest trend.

The U.S. Shale Oil Revolution ?

Indeed, technology advances have made it possible not only for the extraction however debatable with respect to its effects on the environment but also its production.

The International Association for Energy Economics in its report titled ‘Impact of U.S. Shale Oil Revolution on the Global Oil Market, the Price of Oil & Peak Oil’ written by by Mamdouh G. Salameh introduced the subject like this :

“Much has been written about the United States shale oil revolution. Some sources like the International Energy Agency (IEA) went as far as to predict that the United States will overtake Saudi Arabia and Russia to become the world’s biggest oil producer by 2020 and energy self-sufficient by 2030.” This was then in 2012, at the time of this write up of MG Salameh but 5 years on, there seems to be a bis of the same that is on-going.

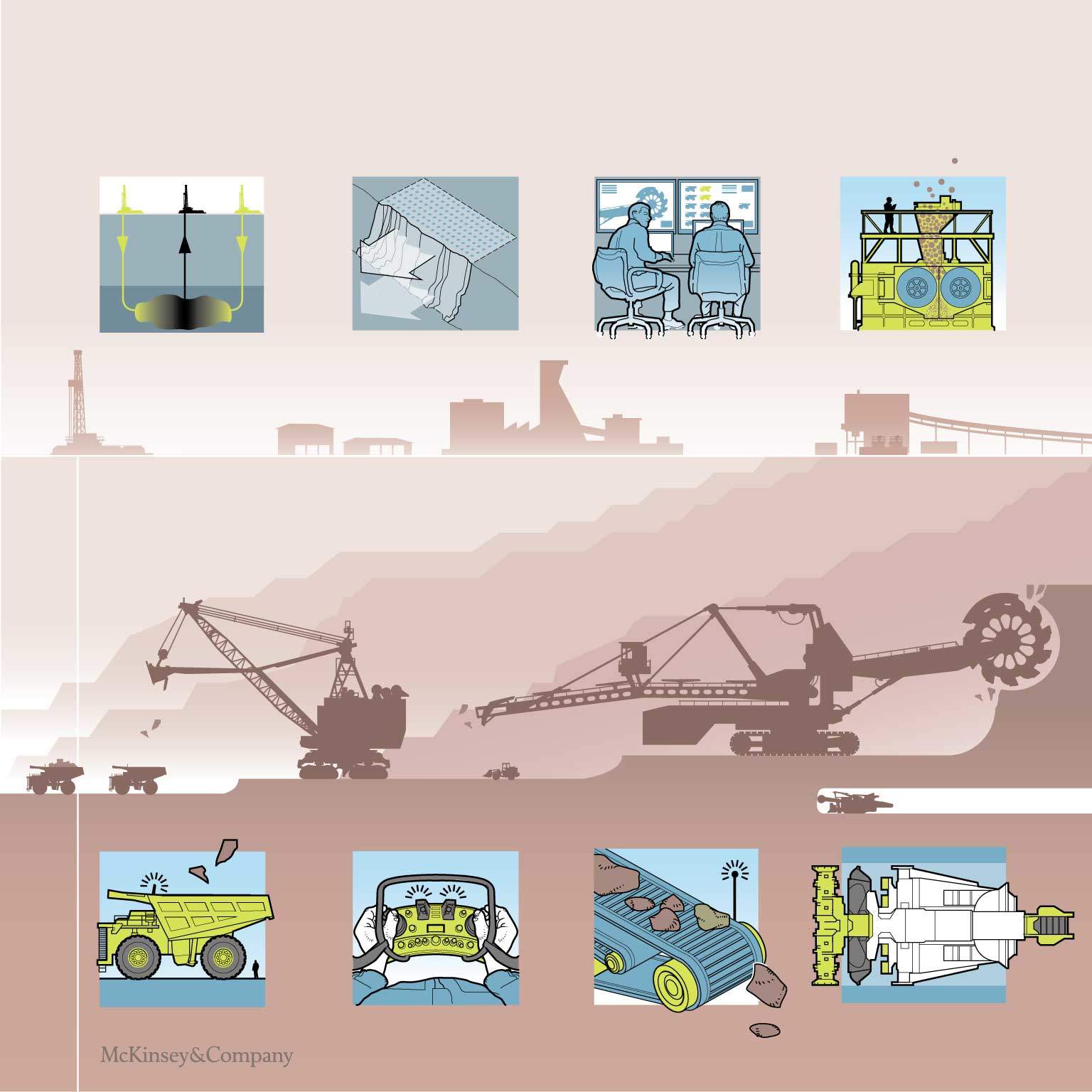

Discover technology’s impact on natural resources

This interactive graphic explores how recent trends could affect supply and demand for resources.

Technological advances are changing the way resources are consumed and produced. This interactive graphic highlights some of the potential changes to both supply and demand for resources. The scenarios depicted should not be considered as specific forecasts but rather as illustrative of the broad trends.

Over the next two decades, we expect energy demand to be reduced in homes, offices, and factories, as well as in transportation, as engines become more fuel efficient and as self-driving and electric vehicles take off. Renewable sources of energy, including wind and solar power, will make major inroads into electricity generation, competing with fossil fuels. For resource producers, data analytics, robotics, and the Internet of Things will bring considerable productivity improvements. To learn more about the impact of ongoing shifts, read the McKinsey Global Institute research report “How technology is reshaping supply and demand for natural resources.”

How technology is reshaping supply and demand for natural resources

By Jonathan Woetzel, Richard Sellschop, Michael Chui, Sree Ramaswamy, Scott Nyquist, Harry Robinson, Occo Roelofsen, Matt Rogers, and Rebecca Ross

The ways we consume energy and produce commodities are changing. This transformation could benefit the global economy, but resource producers will have to adapt to stay competitive.

The world of commodities over the past 15 years has been roiled by a “supercycle” that first sent prices for oil, gas, and metals soaring, only for them to come crashing back down. Now, as resource companies and exporting countries pick up the pieces, they face a new disruptive era. Technological innovation—including the adoption of robotics, artificial intelligence, Internet of Things technology, and data analytics—along with macroeconomic trends and changing consumer behaviour are transforming the way resources are consumed and produced.

On the demand side, consumption of energy is becoming less intense and more efficient as people use less energy to live their lives and as energy-efficient technologies become more integrated in homes, businesses, and transportation. In addition, technological advances are helping to bring down the cost of renewable energies, such as solar and wind energy, handing them a greater role in the global economy’s energy mix, with significant effects for both producers and consumers of fossil fuels. On the supply side, resource producers are increasingly able to deploy a range of technologies in their operations, putting mines and wells that were once inaccessible within reach, raising the efficiency of extraction techniques, shifting to predictive maintenance, and using sophisticated data analysis to identify, extract, and manage resources.

A new McKinsey Global Institute report, Beyond the supercycle: How technology is reshaping resources, focuses on these three trends and finds they have the potential to unlock around $900 billion to $1.6 trillion in savings throughout the global economy in 2035 (exhibit), an amount equivalent to the current GDP of Canada or Indonesia. At least two-thirds of this total value is derived from reduced demand for energy as a result of greater energy productivity, while the remaining one-third comes from productivity savings captured by resource producers. Demand for a range of commodities, particularly oil, could peak in the next two decades, and prices may diverge widely. How large this opportunity ends up being depends not only on the rate of technological adoption but also on the way resource producers and policy makers adapt to their new environment.

Jonathan Woetzel is a director of the McKinsey Global Institute, and Michael Chui is an MGI partner; Richard Sellschop is a partner in McKinsey’s Stamford office; Sree Ramaswamy is a partner in the Washington, DC, office; Scott Nyquist is a senior partner in the Houston office; Harry Robinson is a senior partner in the Southern California office; Occo Roelofsen is a senior partner in the Amsterdam office; Matt Rogers is a senior partner in the San Francisco office; and Rebecca Ross is an associate partner in the London office.

Would you like to learn more about the McKinsey Global Institute? Visit our Natural Resources page

Policy makers could capture the productivity benefits of this resource revolution by embracing technological change and allowing a nation’s energy mix to shift freely, even as they address the disruptive effects of the transition on employment and demand. Resource exporters whose finances rely on resource endowments will need to find alternative sources of revenue. Importers could stock up strategic reserves of commodities while prices are low, to safeguard against supply or price disruptions, and invest in infrastructure and education.

For resource companies, particularly incumbents, navigating a future with more uncertainty and fewer sources of growth will require a focus on agility. Harnessing technology will be essential for unlocking productivity gains but not sufficient. Companies that focus on the fundamentals—increasing throughput and driving down capital costs, spending, and labor costs—and that look for opportunities in technology-driven areas may have an advantage. In the new commodity landscape, incumbents and attackers will race to develop viable business models, and not everyone will win.

{kind=link}